Some of the best low-income students don’t even bother to apply to colleges with the most aid. Why? Blame misleading data.

By Danielle Paquette

ALEXANDRIA, Va. — The teenager stapled together his family’s pay stubs, tax returns and credit card statements. He slid them into his red North Face backpack, between the Advanced Placement calculus textbook and Advanced Placement environmental science binder. Surafel Adere, 17, wished he hadn’t put this off.

All in the name of paying for college.

Figuring out how to pay for a college education has become an exercise in accounting. The College Scholarship Service Profile, a financial aid application that demands nothing short of a family’s financial history, was due in two days. It’s a far more detailed companion to the Federal Student Aid form, which he hadn’t started yet, either. Adere, a T.C. Williams High School senior, had, however, just applied for a full-ride scholarship.

The dogeared tax papers confirmed what he already sensed: His parents, Ethiopian immigrants, struggled beneath debt. The interest alone devoured their budget. He shared a bedroom with his twin brother in a government-owned townhouse.

Fingers crossed. Until he found a sure way to fund school, he’d apply for every way to fund school.

Adere is an exceptional student and is applying for scholarships that could cover all of his college costs. Adere is also an exception: despite his financial situation, he’s applying to top schools, while most high-achieving, low-income students don’t apply to prestigious private colleges. Between 25,000 and 35,000 low-income students score in the academic top 10-percent of all American high-schoolers, according to a Brookings study last year. Many in that group don’t believe they can’t afford tuition or aren’t sure how much aid they’ll receive.

Confusion between a college’s sticker price — the advertised price for fees, board and tuition — and the net price — what students pay after receiving aid — can separate the country’s brightest students from better futures.

“This is despite the fact that selective institutions typically cost them less, owing to generous financial aid, than the two-year and nonselective four-year institutions to which they actually apply,” Harvard public policy professor Christopher Avery and Stanford economics professor Caroline Hoxby wrote.

Adere first received college counseling as a freshman at T.C. Williams. But even the most prepared students, one of his counselors said, can get stuck in the financial aid mire.

“There are a lot of students who say, I can only go to school in-state because that’s all we can afford,” said Marianne Hetzer, director of Building Better Futures, which offers financial aid tutoring to students at T.C. Williams. “The information can come from parents or the cultural idea that in-state is always cheaper.”

The college application process is already intimidating, Hetzer said. A student who knows his family struggles financially may write off a school before visiting its Web site. The average sticker price for a private, non-profit four-year college — including tuition fees and room and board — was $40, 920 last year, according the College Board. But the net price after aid and grants was estimated to be roughly $23, 290.

Most days, Adere works after school at a local retirement home. Poring through his family’s tax records was an unwelcome diversion. He’d rather be at a movie with his friends. Or listening to Drake, his favorite way to unwind.

But only discipline, Adere knew, would get him into Princeton, his dream school. Discipline to maintain his 4.2 GPA. Discipline to figure out how he could afford it.

He stepped into T.C. Williams’ college career center, wary to share these intimate worries and numbers with the outside world. His parents, who attended school in Ethiopia, didn’t understand the financial aid process — or why he needed a recent W-2 form. “Do you not trust us with money?” his father had asked.

Adere handed the paper stack to a guidance counselor.

“I need to get this done today.”

**

College aid shrinks or swells, depending on who’s applying, where they’re applying and how well they navigate the financial aid systems. The federal government offers tools to help students decide what they can afford, but they’re often confusing. The College Navigator, for example, aims to show how much, on average, students from different financial backgrounds pay to attend different colleges. The Department of Education annually lists the most affordable and most expensive schools.

The information online is likely accurate — but that doesn’t mean it’s helpful, Wellesley College economics professor Phillip Levine argues in a Brookings Institution paper released today. The government numbers, Levine writes, are too broad to inform a student’s specific financial situation.

“Evidence indicates that the majority of students know no price other than the stated level of college tuition,” Levine wrote, “despite the fact that many students would be expected to pay far less than that.”

This sticker price illusion keeps talented teenagers from applying to their dream schools, experts say. Student debt fears may also drive them to choose what they deem cheaper options.

Levine, who monitors tuition transparency at Wellesley, first noticed the problem in August. A reporter called him, asking: Why has tuition cost tripled over the last few years for your low-income students? The reporter, he said, got that information from the government’s College Navigator.

An investigation by Wellesley showed the site’s numbers were accurate — but skewed. Each year, about 2,400 students attend the private liberal arts school in Massachusetts, which has needs-blind admission and a $1.8 billion endowment. More than half receive some financial aid.

Most Wellesley students who reported household incomes of less than $30,000 paid just a tenth of the college’s sticker price of $50,000. A handful in this low-income group, however, was set to pay full price tuition.

The students who paid sticker price came from “unusual situations,” Levine said. One, for example, was retired with no income — but substantial assets. “Those few students completely skewed the results,” he said. “That is not useful information and, indeed, is detrimental to report to students from low-income families.”

The result: High school seniors considering Wellesley may Google “tuition cost” and promptly back away. If it was happening at Wellesley, Levine reasoned, it could happen anywhere.

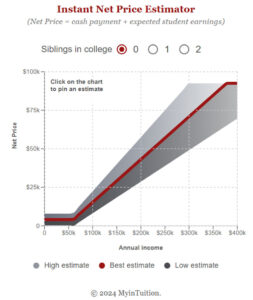

To fix the problem, the school released this year the My InTuition calculator, which asks prospective students more specific questions and provides a personally tailored aid estimate. The applicant pool, Levine said, increased by 20-percent. He’s asking for a similar calculator to be made national.

“Don’t stop when you see the sticker price,” he said. “Get started early. Understand all your options.”

Adere, despite his parents’ financial situation, never looked at Princeton’s pricetag. He hoped the mish-mash of scholarship and financial aid applications returned a significant discount — or, at least, a number easier to stomach.

“Teachers always told me I’d get there by merit,” he said. “So, I always believed I’d get there by merit. I told myself I’d just go for it.”

**

Trudging to the guidance counselor’s office, Adere craved coffee. He had stayed up past midnight solving Calculus sets. Math was easy until this year. Now, it required more effort.

That could be mental fatigue, he figured. Most days, homework didn’t start until 8 p.m., after a four-hour shift at a local retirement home. The paychecks covered his khaki pants, his Polo shirts, his sartorial message to the world: I’m polished and professional.

He sat in the college career center with a counselor for four hours, scrutinizing each page.

This is so annoying, Adere thought.

College flags dangled from the wall: University of Virginia, Georgetown, George Washington University… Adere imagined Princeton colors, orange and black. His Polo collection would be updated accordingly.

He applied in October. The plan: Study mechanical engineering, build a robot that will cut lawns, someday take the financial burden off his mother.

Years ago, she earned her associate’s degree in Ethiopia. She became a manager at the Ronald Reagan Washington National Airport. Her husband, who never graduated from high school, juggled valet jobs.

They wanted more for their son.

An e-mail last month eased Adere’s anxiety, the first fruit of his financial aid labors. It wasn’t from the College Board. It wasn’t from the Department of Education. It wasn’t from Princeton, which likely won’t send him an answer until December.

It was from Questbridge, a charity that connects low-income students to highly selective schools. Adere was eligible for the full-ride scholarship — applicable to 35 schools in the country, including Princeton, and contingent on whether or not he gets in.

Discipline paid off, Adere told his mother. He’ll finish all the financial aid applications, though — just in case.

(Haven’t saved a dime for college? Find out what to do here.)

*The percentage increase of Wellesley applicants has been corrected in this article.

As seen: https://www.washingtonpost.com/news/storyline/wp/2014/11/12/student/?utm_term=.bab9da84a9b0